DALLAS, TX -- July 28th, 2023 -- Plumas Bancorp (Nasdaq: PLBC): Stonegate Capital Partners updates coverage on Plumas Bancorp (Nasdaq: PLBC). The full report can be accessed by clicking on the following link: Plumas Bancorp Q2 2023 Report

Company Summary

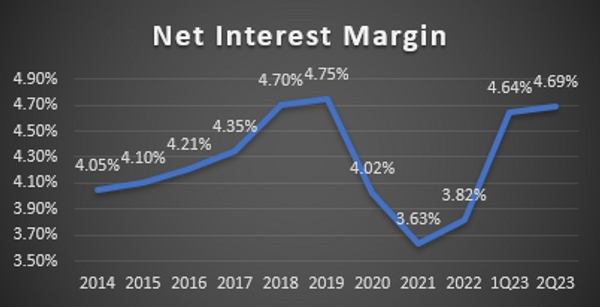

- Maintained Strong Position: Compared to a strong 2022, assets decreased slightly to $1.57B at 2Q23 end, down from $1.62B at 2Q22. Deposits also decreased to $1.40B in 2Q23 from $1.47B in 2Q22. Investment securities have grown by $104M Y/Y to $469M. The Company’s loan to deposit ratio was at a healthy 67.0%. For the first six months PLBC has recorded record earnings thanks in large part to strong net interest income and NIM. This growth has culminated in the Company being included in the R2000 Index.

- Community banks on strong footing: In the wake of the SVB failure there has been increased scrutiny on the banking sector. When compared to larger regional banks, we believe that local banks like PLBC are better suited to weather this bank sector turmoil. This is in large part due to community banks having less than 10% of their accounts uninsured by the FDIC as compared to SVB’s 95% of accounts being uninsured. It is also notable that SVB had a much lower NIM, at 2.0% in 4Q22, as compared to PLBC at 4.69% in 2Q23. Additionally, assets at PLBC have shorter durations compared to peers and they are not invested in held-to-maturity securities.

- Strong core deposits: Plumas has a strong history of increasing its demand, savings, and money market deposits from local businesses and individuals. However, deposits fell by $77.4M Y/Y to $1.40B on June 30, 2023. This decline is attributed to the increasing rate environment. Despite this headwind, the Company has grown deposits at a ~17% CAGR since 2018.

- Diversified loan portfolio: PLBC provides a range of lending services with the breadth of loan diversification helping Plumas to avoid becoming overly concentrated in a single industry. As of 2Q23 79% of the loan portfolio was comprised of variable rate loans. The Company saw gross loans increase by 9% from $862M in 2Q22 to $935M in 2Q23.

- Non-interest earnings income growth: In addition to the Company’s primary source of revenue, interest income, in 2Q23 Plumas also derived ~$2.14M of its revenue from a variety of noninterest income items including loan servicing fees, service charges on deposit accounts, interchange revenue, and gains on sales of SBA 7a loans.

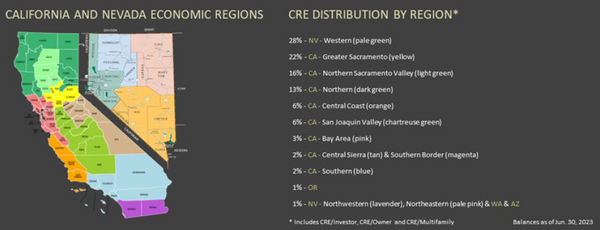

- Successful growth strategy: The Company continued to expand its branch operations into targeted growth markets of Northern California and Northwestern Nevada over the years with great success including the purchase of Mutual of Omaha Bank’s Carson City Branch in October 2018 and the acquisition of Feather River Bancorp in 2021. Most recently the company opened its Chico, California branch in 2Q23.

- Valuation: We use a comp analysis on P/E and P/BV to help frame valuation. Using a P/E range of 7.5x to 8.5x with a mid-point of 8.0x on our FY24 EPS estimate results in a valuation range of $38.89 to $44.07 with a mid-point of $41.48. Using a P/BV multiple range of 1.7x to 2.1x, we arrive at a valuation range of $37.27 to $46.04 with a mid-point of $41.65. Additional details can be found on page 9.

About Stonegate Capital Partners

Stonegate Capital Partners is a Dallas-based corporate advisory firm dedicated to serving the specialized needs of small-cap public companies. Since our inception, our mission has been to find innovative, undervalued public companies for our network of leading institutional investors who seek high-quality investment opportunities.

Stonegate Capital Partners is a Dallas-based corporate advisory firm dedicated to serving the specialized needs of small-cap public companies. Since our inception, our mission has been to find innovative, undervalued public companies for our network of leading institutional investors who seek high-quality investment opportunities.