DALLAS, TX -- July 31st, 2023 -- Civeo Corporation (NYSE: CVEO): Stonegate Capital Partners updates their coverage on Civeo Corporation. The full report can be accessed by clicking on the following link: Civeo Q2 2023 Report

COMPANY UPDATES

- Significant Free Cash Flow Generation: The Company continues to maximize its generation of free cash flow. Civeo has been free cash flow positive every year since 2014 and is expected to maintain positive FCF going forward. After posting a negative FCF in 1Q CVEO became FCF positive YTD from $12.9M in 2Q free cash flows. CVEO updated its FCF guidance for the year to $48.0M to $58.0M with a midpoint of $53.0M.

- 2Q23 Results In-Line: CVEO reported revenue, adj EBITDA, and adj EPS of $178.8M, $31.6M, and $0.30, respectively. This compares to our/consensus estimates of $168.4M/$173.6M, $28.8M/$26.4M, and $0.30/$0.31, respectively. Revenue was higher than expectations, driven by strength in the Australian market and greater than expected billed rooms. GPM was also above our expectations by ~150bps. Despite this, profitability was in-line with expectations after tax rates came in higher than modeled.

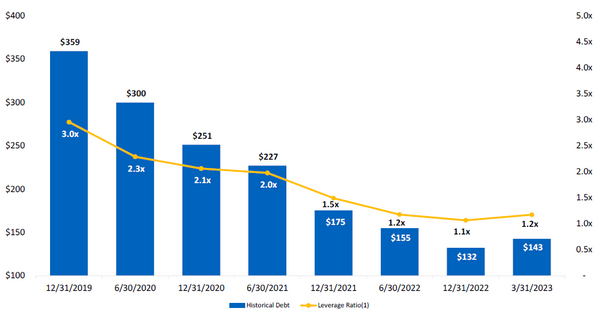

- Capital Allocation: In 2022 Civeo initiated a share repurchase program as part of its plan to return capital to shareholders. CVEO continued to return capital through share repurchases in 2Q23 with 212,000 shares repurchased for an approximate value of $4.2M. Additionally, the Company used cash to decrease debt by $6.5M Q/Q to $136.1M. This translates into a net leverage ratio of 1.2x. Management has indicated that a formal policy for capital allocation can be expected by the end of 2023. CVEO ended the quarter with $77.6M in revolver availability and $11.4M in cash for $89.0M in liquidity.

- Canadian Market: With the upcoming construction wind down of the TMX and Coastal GasLink pipelines, Civeo will begin demobilizing its mobile camps starting in 2H23 and into 2024. The Company will incur demobilization costs of $10M in 2023 and $6M in 2024, which will significantly impact EBITDA. CVEO is also dealing with the sale of their McClelland Lake asset. Management announced that they are in negotiations for this sale, with more information expected by 3Q23.

- Room Rates: The Canadian segment saw a decrease in its average daily room rates from $103 in 2Q22 to $100 in 2Q23. while the Australian segment saw a narrower decline, dropping from $77 in 2Q22 to $75 in 2Q23. The movements in roommates were affected by the weakening of the Australian and Canadian dollars compared to the U.S. dollar. This was buoyed by the Australian segment seeing a 30% Y/Y revenue increase on a constant currency basis.

- Guidance Update: Current 2023 EBTIDA guidance is in range of $90M to $95M, a raise from $85M to $95M last quarter. Given the relative uncertainty for demand from customers doing turnaround work, we have modeled EBITDA towards the midpoint of guidance.

- Valuation: We use both a DCF and EV/EBITDA comp analysis to guide our valuation. Our DCF analysis produces a valuation range of $27.97 to $33.99 with a mid-point of $30.59. Our EV/EBITDA valuation results in a range of $27.45 to $33.33 with a mid-point of $30.39.

About Stonegate Capital Partners

Stonegate Capital Partners is a Dallas-based corporate advisory firm dedicated to serving the specialized needs of small-cap public companies. Since our inception, our mission has been to find innovative, undervalued public companies for our network of leading institutional investors who seek high-quality investment opportunities.

Stonegate Capital Partners is a Dallas-based corporate advisory firm dedicated to serving the specialized needs of small-cap public companies. Since our inception, our mission has been to find innovative, undervalued public companies for our network of leading institutional investors who seek high-quality investment opportunities.