DALLAS, TX -- October 31st, 2024 -- Aquafil Group (ECNL.MI): Stonegate Capital Partners updates coverage on Aquafil Group (ECNL.MI). In 3Q24, ECNL observed continued improvement within the macro environment in both EMEA and Asia markets, with volumes growing year over year and aligning with company expectations. The Company experienced volume headwinds in North America, but signs of recovery were noted in both fiber product lines despite the impacts of Hurricane Helene in North Carolina. We expect that volumes in North America will increase through the balance of FY24 and into early FY25. On a consolidated basis, ECNL reported improved EBITDA margins compared to 3Q23 despite lower revenue. This improvement is partly due to the increasing percentage of ECONYL® sales, which accounted for 56.7% of revenues generated from fibers in the third quarter. The Company also remains focused on debt repayment with a decreasing trend in net financial position, as evidenced by the NFP/EBITDA ratio improving to 4.52x at the end of 3Q24 from 5.23x at the end of FY23. Lastly, ECNL’s capital increase operation to further support the Business Plan is expected to be completed by the end of the current year.

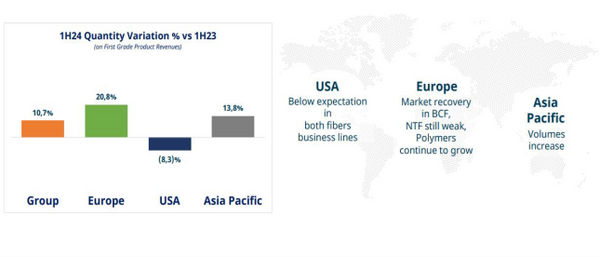

- Quarterly results: ECNL reported revenue, adj EBITDA, and adj EPS of €131.3M, €15.5M, and (€0.05), respectively. This compares to our/consensus estimates of €152.1M/€150.2M, €16.6M/€16.1M, and (€0.06)/(€0.06), respectively. Revenues were impacted by a 6.3% increase in volumes sold during the first nine months, which wasn't entirely backed by selling prices due to their adjustment to the lower cost of raw materials and changes in the sales mix, primarily seen in the North American market. Volumes saw a rebound y/y in both Asia and EMEA. This resulted in a y/y revenue decline of 1.8%. GPM was ahead of our expectations as the Company has worked diligently to reduce costs. EBTIDA margin was 11.8% in the quarter, compared to 4.2% in 3Q23.

- Outlook: The Company is optimistic about growth through 2025, addressing short-term challenges with cost-cutting measures and a covenant holiday from lenders for FY24, while benefiting from rising volumes in EMEA and Asia. Profitability has significantly improved in the first nine months, with third-quarter EBITDA margins exceeding 11%, alongside a notable improvement in the net financial position and NFP/EBITDA ratio. Demand in the Asia Pacific and EMEA regions has met budget forecasts, and the U.S. market is showing signs of recovery in fibers despite Hurricane Helene's impact. We anticipate continued profitability improvements and rising volumes in the fourth quarter.

- ECONYL® Expansion on Track: The Company reported another quarter of strong ECONYL® contributions to revenues at 56.7% for 3Q24. This is an increase of 390 bps from 52.8% seen in 2Q24. Sales seem to be buoyed by the European market which has been swift to adopt, with the North American market finally observing traction despite market headwinds. We expect the North American market to see a rebound over the remainer of FY24. This level of ECONYL® contribution to revenue is in-line with management’s expectations and is expected to remain a positive addition to the financials, with the goal of reaching 60% by FY25.

- Valuation: We use both a DCF Model and EV/EBITDA Analysis to frame our valuation of ECNL. Our DCF analysis relies on a range of discount rates between 10.75% and 11.25%. This arrives at a valuation range of €4.33 to €4.86 with a mid-point of €4.59. Our EV/EBITDA analysis relies on a range of 5.5x to 6.0x leading to a valuation range of €4.16 to €5.02, with a midpoint at €4.59.